Berkshire Hathaway is one of the world’s premier investment conglomerates. Through strategic investments, subsidiary businesses operating in insurance and logistics, and a disciplined business approach, it has grown to a nearly $800 billion company.

Led by Warren Buffett and his team, Berkshire Hathaway and its investments have influenced countless investors globally. Still, copying Berkshire’s portfolio, stock for stock, may not be the best option because your goals and risk tolerance may not entirely align with it.

However, for investors looking for Berkshire Hathaway stocks to load up on now, here are three that are well worth considering.

1. Coca-Cola

Coca-Cola (NYSE: KO) has been a staple in Berkshire Hathaway’s portfolio since its first investment in 1988. Since then, Berkshire Hathaway has accumulated 400 million Coca-Cola shares, representing around 9% of the company’s shares.

In the U.S., Coca-Cola had a 46% market share in the carbonated soft drink market at the end of 2022, far outpacing its biggest competitor, PepsiCo. Regardless of Coca-Cola’s market dominance over the decades, I appreciate how it has yet to get complacent and continues prioritizing innovation and adapting to consumers’ ever-changing preferences. A testament to this has been Coca-Cola’s Transformational Innovation Team, whose sole purpose is driving product development and exploring new market trends.

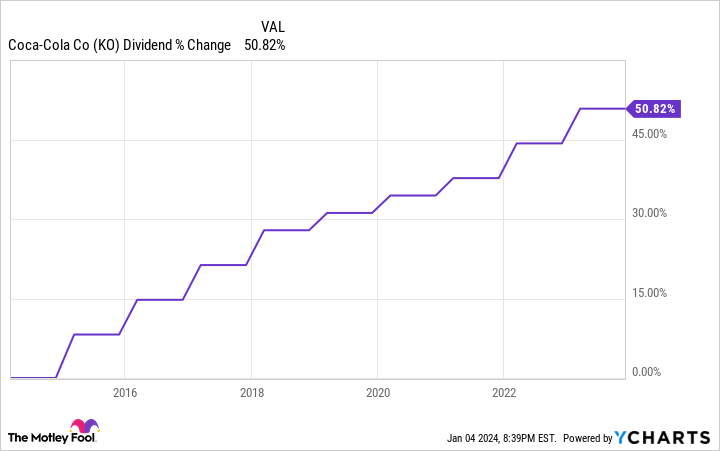

Coca-Cola’s stock price has underperformed against the S&P 500 over the past decade, but its dividend is what generally attracts investors. Coca-Cola’s quarterly dividend is $0.46, with a trailing 12-month yield of around 3%. Arguably more impressive is that it has increased its yearly dividend for 61 consecutive years, giving it the esteemed title of Dividend King. In the past 10 years alone, Coca-Cola’s quarterly dividend has increased by over 50%.

Coca-Cola isn’t a growth stock that’ll consistently return double-digit percentages year in and year out, but it can provide investors with as reliable a dividend as you’ll find on the stock market.

2. Visa

Visa (NYSE: V) is the global leader in digital payments, with a vast, constantly expanding reach. It operates in over 200 countries, has over $4.3 billion cards in circulation, and is accepted by over 130 million merchant locations.

Visa’s reach is its key competitive advantage, mostly because of the network effect. Imagine you’re a retailer and have to choose which cards you’ll accept. Chances are high that you’ll go with Visa because you understand your customers will likely have a Visa card over other options. Not accepting Visa cards could mean missing out on sales. The same applies to consumers looking to get a card. Many prefer a Visa card because businesses that accept cards are very likely to accept Visa.

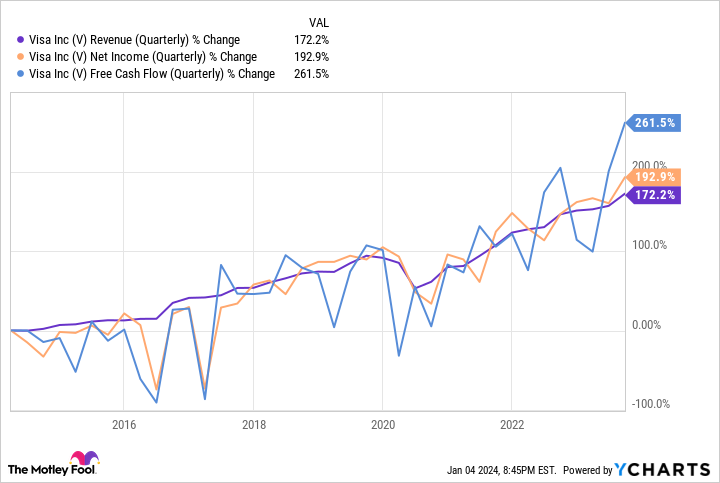

Visa’s recent growth has translated well to its financials as well. Over the past decade, its revenue is up 172%, but its net income and free cash flow have grown faster, signaling the company is operating more efficiently.

The U.S. may be a leader in digital payments, but

kebo88 | slot gacor | situs slot gacor

much of the world still operates in a cash economy. That gives Visa plenty of market opportunity as countries transition toward digital and electronic payments. It’s a stock I feel comfortable holding onto for the long haul.

3. Amazon

Amazon (NASDAQ: AMZN) isn’t a company that needs much of an introduction. Its e-commerce business has made it a household name around the globe. However, it likely won’t be Amazon’s e-commerce business that drives a lot of its growth in the foreseeable future — it may be the logistics network that powers it.

Amazon recently announced “Supply Chain by Amazon,” a fully automated set of supply chain services. The service allows sellers to take advantage of Amazon’s complex logistics, warehousing, distribution, fulfillment capabilities, and transportation (including international).

Amazon has spent billions building out its logistics network, and Supply Chain by Amazon allows the company to capitalize from it outside of its core e-commerce business.

E-commerce will continue to be Amazon’s main revenue driver, and Amazon Web Services will be its main profit generator, but it’s encouraging to see other segments beginning to pull their own weight a little more. In the third quarter of 2023, Amazon’s third-party seller services revenue grew 20% year over year (YOY). Advertising led the way, growing 26%.

Amazon has its hands in many high-growth industries, so there should be plenty of value to be returned to shareholders as the company continues to expand across industries.

Should you invest $1,000 in Berkshire Hathaway right now?

Before you buy stock in Berkshire Hathaway, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Berkshire Hathaway wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 18, 2023

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Berkshire Hathaway, and Visa. The Motley Fool recommends the following options: long January 2024 $47.50 calls on Coca-Cola. The Motley Fool has a disclosure policy.

3 Berkshire Hathaway Stocks to Buy Hand Over Fist in January was originally published by The Motley Fool

{kind=link}