:-turning-into-a-free-cash-flow-powerhouse")

As a Palantir (NYSE:PLTR) shareholder, I couldn’t be happier with its ~35% post-earnings surge. The AI-driven data analytics and intelligence software company impressed investors, highlighting strong traction in bootcamps, growing AIP (Artificial Intelligence Platform) adoption, and improving profits. Management expects continued acceleration in its Commercial division. In the meantime, Palantir is gradually turning into a free cash flow powerhouse.

That said, while I will remain invested in Palantir for its long-term prospects, I have now adopted a neutral stance following the stock’s massive gains.

Bootcamps Driving Explosive Commercial Growth

One of the highlights of Palantir’s Q4 report was how the company was able to drive explosive growth in its Commercial division. Just to break it down a bit, Palantir’s business is split into two parts: Government (bringing in 53% of revenues) and Commercial (raking in the other 47%). Now, while the Government side is still growing rather rapidly, posting 11% growth in Q4, the real excitement is brewing in Palantir’s Commercial division.

Indeed, Palantir’s Commercial division far outperformed its Government business, growing revenues by 32% year-over-year. This was driven by a massive 55% increase in Palantir’s customer count to 221 firms. The rapid client success here can be attributed to Palantir’s implementation of a highly demonstrative customer acquisition strategy- bootcamps.

What Are Bootcamps All About?

Palantir’s bootcamps serve as intensive, hands-on workshops designed to showcase the capabilities of their products, particularly Palantir’s AIP.

Palantir’s strategy here literally involves cold-approaching CEOs and CTOs, urging them to put their best AI teams to the test. In Palantir’s words, such an approach usually sounds like this:

Take everything you’ve done in AI, put your best people on it, and we’ll run your data at a 10-hour bootcamp. Compare your results to our operationally-relevant, commercially-valuable outcomes. Our 10 hours versus your 10 months. Any products, vendors, or hyperscalers you choose, we’ll be there.

Q4 Earnings Call

Sure enough, many executives have shown interest in trying out Palantir’s platform, especially given the buzz Palantir has gathered in the tech space. The demand for these immersive “workshops” has surged so that Palantir has not only met but surpassed previous expectations. Palantir has conducted an impressive 560 sessions since October, a feat that already exceeds their initial goal of 500 within the span of a year.

The Effect of Bootcamps on Revenue Growth

Palantir’s bootcamp strategy has played a crucial role in driving revenue growth within the Commercial division and company-wide. In fact, Palantir’s management highlighted that the company has secured significant deals through this approach. Witnessing firsthand the tangible results that Palantir can deliver for businesses, other business executives are compelled to embrace this transformative technology, recognizing it as an opportunity they cannot afford to overlook.

Just to name a few, Palantir signed deals:

-

Exceeding $25 million each, with

-

one of the largest car rental companies, one of the largest telecommunication companies, and one of the largest pharmaceutical and biotechnology corporations in the world.

-

-

Exceeding $10 million each, with

-

an American consumer packaged goods holding company, an American automotive seat and electrical systems manufacturer, a comprehensive health network in the Midwest, and a large-scale battery manufacturer.

-

-

Exceeding $5 million each, with

-

an American bank holding company, a horse racing regulatory organization, one of the world’s largest equipment rental companies, and one of the largest independent non-profit cooperatives in the QSR space.

-

And these are just a few of the examples.

The bar chart below from Palantir’s Q4 presentation clearly illustrates the success of bootcamps in driving commercial customer count. Specifically, on a trailing-12-month (TTM) basis, Palantir’s Commercial customer count grew by 22% quarter-over-quarter. This implies a fantastic acceleration compared to the equivalent figures of 8%, 4%, and 12% achieved in Q1, Q2, and Q3, respectively.

Given such impressive momentum in Palantir’s Commercial customer count, it’s pretty clear that Wall Street is likely pricing a scenario of accelerating revenue growth in the coming quarters. Palantir’s management itself

kebo88 | slot gacor | situs slot gacor

has substantiated this expectation by providing guidance for U.S. Commercial revenue surpassing $640 million in FY2024, indicating a growth rate of at least 40%. This further reinforces the optimism surrounding the company’s trajectory.

Palantir: Generating Free Cash Flow, but Valuation Concerns Emerge

With strong revenue growth of 20% to $608 million across Government and Commercial in Q4, Palantir is gradually enjoying improving unit economics and turning into a free cash flow machine.

To add some color regarding Palantir’s profitability overall, the company’s adjusted operating margin jumped to 34% in Q4, up from 22% in the previous year. This marked the fifth consecutive quarter of expanding adjusted operating margins and the fifth straight quarter of positive GAAP net income.

GAAP net income landed at $93 million, representing a 15% margin. Yes, Palantir is now very profitable, even on a GAAP basis, and margins have only started expanding. Sure, this $93 million includes $44.5 million interest income from its $3.7 billion cash position, but profits are profits, especially given that this is on a GAAP basis.

But let me go back to free cash flow, which came in at $305 million on an adjusted basis, representing a 50% margin. Note that this figure includes $132.6 million in stock-based compensation (SBC) expenses and thus should be taken with a grain of salt. That said:

-

a) Even excluding SBC, it represents a massive free cash flow margin of 25%+.

-

b) It shows the extreme potential for Palantir’s free cash flow to grow as its overall margins expand.

-

c) Total SBC actually declined year-over-year in FY2023, which is certainly encouraging.

Management’s guidance, in fact, indicates this potential, as it expects adjusted free cash flow to come in between $800 million and $1 billion. I believe this estimate is highly conservative, given the undeniably incredible momentum Palantir finished FY2023 with and current margins, which are poised to keep expanding from here.

In any case, even these numbers showcase how fast Palantir is turning into a free cash flow powerhouse. For context, two years ago, in FY2022, adjusted free cash flow was only $203 million.

Has Palantir Stock Gotten Too Pricey?

Despite Palantir’s operational excellence, it’s hard to ignore that shares might have become too pricey. At 51 times the high end of management’s adjusted free cash flow guidance range for this year, no further proof is needed to say that Palantir is trading at a massive premium.

While exponential growth in the medium term could eventually justify paying this multiple today, you should expect significant volatility in the stock price. Because of the now notably thinner margin of safety compared to prior quarters, I have changed my stance on the stock from bullish to neutral.

Is PLTR Stock a Buy, According to Analysts?

The current sentiment on Wall Street appears somewhat more reserved following the stock’s massive gains. According to Wall Street, Palantir Technologies features a Hold consensus rating based on three Buys, five Holds, and five Sells. in the past three months. At $18.20, the average PLTR stock price target suggests 25.35% downside potential.

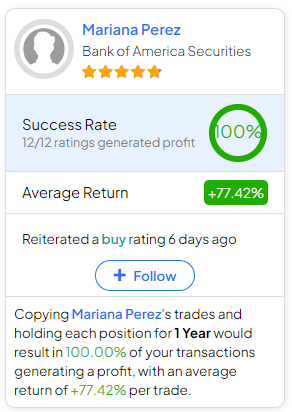

If you’re wondering which analyst you should follow if you want to buy and sell PLTR stock, the most profitable analyst covering the stock (on a one-year timeframe) is Mariana Perez from Bank of America Securities, with an average return of 70.89% per rating and a 100% success rate. Click on the image below to learn more.

The Takeaway

Palantir’s Q4 performance, powered by its impactful boot camps and growing demand for its product, has propelled the stock to impressive gains. As a shareholder, I couldn’t be happier with the recent gains.

Based on management’s guidance, the Commercial division’s phenomenal revenue growth is set to accelerate even further. In the meantime, given the company’s high-margin business model, Palantir’s free cash flow generation shows immense potential. I will continue to hold the stock for these reasons and the fact that I see Palantir dominating the AI-powered decision-making software space.

However, despite these positive indicators, the stock’s pricey valuation raises concerns. As a shareholder, I remain optimistic about Palantir’s long-term potential, but considering the recent surge, I have shifted to a neutral stance, lowered my expectations, and prepared for increased volatility ahead.

{kind=link}